Best Payment Infrastructure APIs for SaaS Embedded Payouts (March 2026 Update)

Your marketplace needs to let sellers cash out instantly, your gig app wants to pay drivers daily, and your affiliate network is running commissions across 50 countries. Building that payment infrastructure yourself means months of bank onboarding, compliance workflows, and tax filing logic. We ranked the top embedded payout APIs on five criteria: how many countries they serve, whether they support real-time rails, how fast your team can go live, whether they handle KYC and 1099s automatically, and if their FX spreads are disclosed upfront or buried in the fine print.

TLDR:

- Embedded payout APIs let SaaS platforms send money to contractors and users through code

- Dots supports 300+ rails across 190 countries with real-time settlement and no instant fees

- Most providers cap coverage at 46 countries or charge 1-2% extra for instant payouts

- You can go live in under a week vs 4-12 weeks with traditional AP automation tools

- Dots offers white-label onboarding, automated tax filing, and 24/7 recipient support

What Are Embedded Payout APIs?

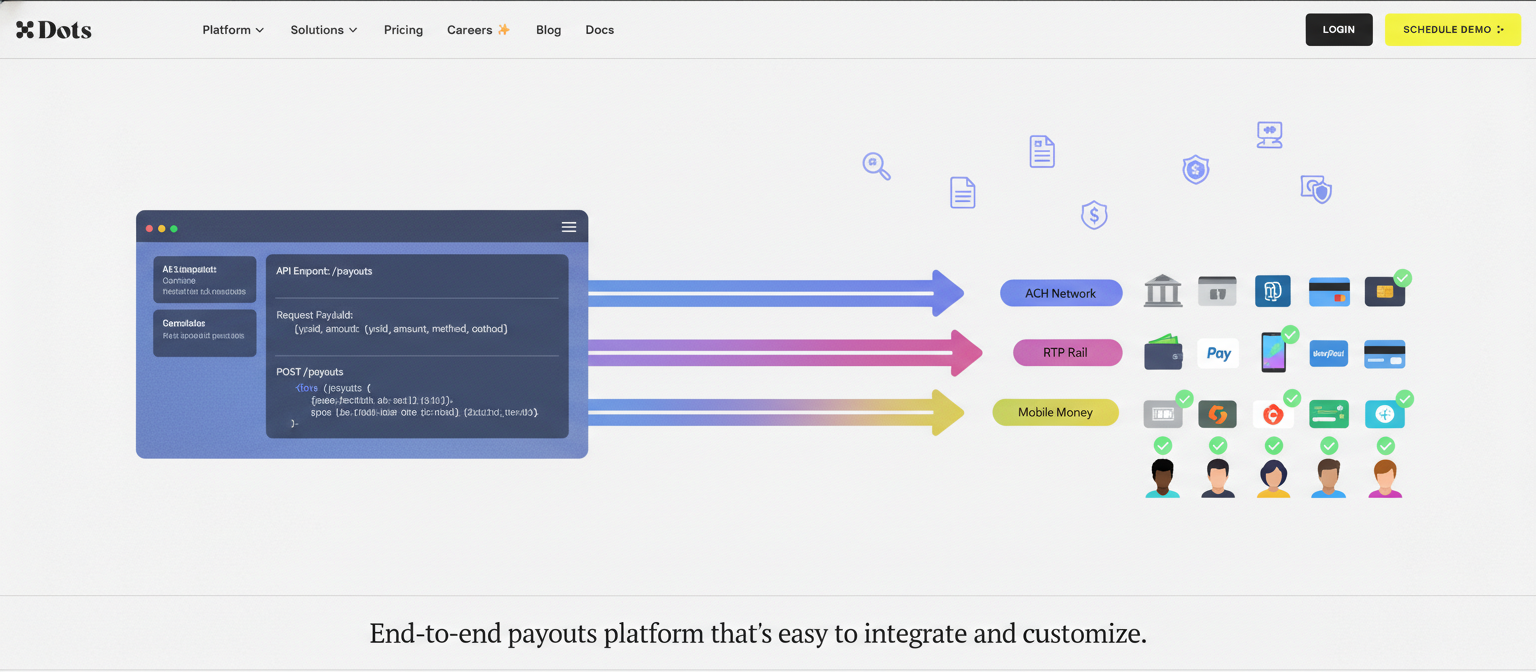

Embedded payout APIs are developer tools that let SaaS companies send money to contractors, sellers, and users through a few lines of code. Instead of building payment rails, bank integrations, and compliance workflows yourself, you call an endpoint and the API handles verifying payee identities, routing funds across ACH, RTP, mobile money, or digital wallets, filing tax forms, and tracking transaction history.

These APIs turn disbursements into a product feature instead of a back-office headache. A marketplace can let sellers cash out instantly, a gig app can pay drivers daily, and an affiliate network can automate commission runs across 50 countries.

Embedded payout APIs fit into the broader shift toward embedded finance, where SaaS applications weave financial services directly into user workflows. Payments stop being a bolt-on and start driving retention, revenue share, and faster time to market.

How We Ranked Embedded Payout APIs

We tested each API against five criteria that matter when you're choosing a payout partner:

- Global coverage and payment rails: How many countries can you serve, and can payees pick local methods like UPI, PIX, or mobile money instead of just bank transfers?

- Settlement speed: Does the API support real-time rails (RTP, FedNow) or do payees wait days for ACH batches?

- Developer experience: How clean is the API documentation, and how fast can your team go live?

- Compliance automation: Does the vendor handle KYC, tax filing, and fraud checks, or do you build that yourself?

- Transparent pricing: Are FX spreads and instant payout fees disclosed upfront, or hidden in the fine print?

Our rankings draw from public documentation, vendor sites, and user reviews. As embedded payments become a retention lever, picking the right API can turn payouts from a cost center into a growth driver.

Best Overall Embedded Payout API: Dots

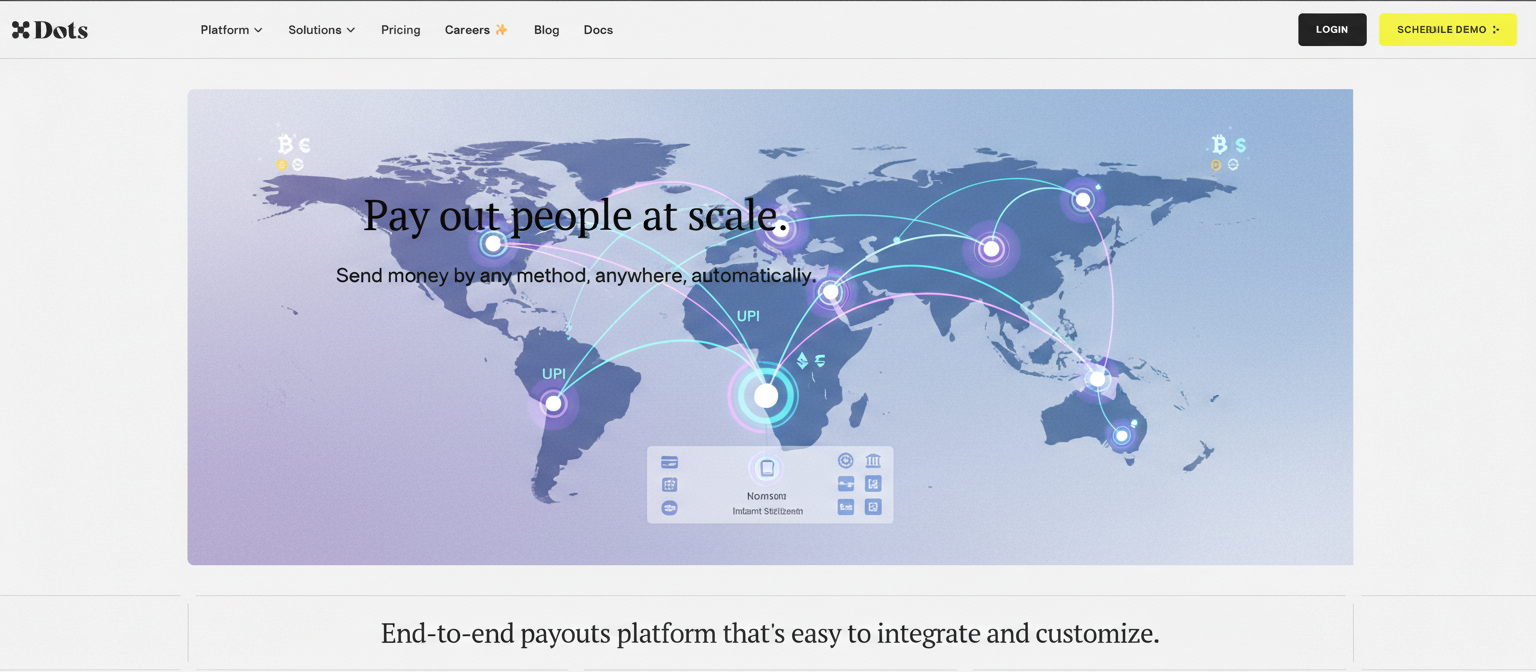

Dots delivers global payout coverage across 190 countries and 300 rails, including RTP, FedNow, UPI, PIX, mobile money, and digital wallets, so payees receive funds in seconds via real-time networks or within 48 hours for cross-border transfers. Our unified payouts API handles everything out of the box. Pricing is transparent: $999 monthly, flat domestic fees, percentage-based international fees at mid-market FX rates, and zero instant-payout surcharges.

You get white-label onboarding, 24/7 recipient support, automated 1099 filing, and KYC/AML screening out of the box. Our instant payouts deliver funds in seconds. API docs mirror Stripe's design, putting your team live in under a week. While most providers cap coverage at 46 countries or rely on slow ACH batching, Dots bundles real-time speed and global reach in one contract.

Tremendous

Tremendous is a digital rewards and incentives solution that specializes in gift cards, prepaid Visa cards, and cash disbursements to over 200 countries. The API automates reward distribution for research studies, loyalty programs, and employee recognition.

What they offer

- Over 1,000 redemption options including gift cards, prepaid cards, and PayPal/ACH cash. Recipients choose how they want to receive value, whether through retail gift cards, prepaid Visa options, or direct cash transfers.

- API for automated reward distribution at scale. Send single or bulk payments programmatically, eliminating manual processing for incentive programs.

- Free to use with no monthly fees. Pay only for the value you send, making it cost-effective for occasional or seasonal reward campaigns.

- Dashboard tracking and bulk sending capabilities. Monitor redemption rates and manage large recipient lists through a web interface.

Tremendous works well for companies running research studies, customer loyalty programs, or employee recognition that need flexible gift card and incentive options instead of instant payouts infrastructure for contractors.

The catch: Tremendous is built for incentives and rewards, not day-to-day contractor payouts. You won't find native support for instant local rails like RTP, UPI, or PIX that contractors expect. White-label capabilities are also limited compared to payout-first infrastructure.

Routable

Routable is an accounts payable automation tool that helps finance teams process vendor invoices and batch payments through bank transfers, wires, and ACH.

What they offer

- Automated invoice capture and approval workflows that route bills through multi-step finance team review processes

- API for programmatic payables integration with accounting systems like NetSuite and Sage Intacct

- Batch CSV payments and vendor onboarding tools built for finance operations

- Bank transfer and ACH rails for scheduled vendor disbursements

Routable works best for finance teams managing traditional vendor payments who need invoice-to-payment automation tied to accounting software. The trade-off: Routable focuses on AP automation instead of developer-first embedded payouts. For teams building payout features directly into their product, specialized solutions work better. You won't find instant payment rails like RTP or FedNow, and implementation takes longer compared to payout-specific APIs built for SaaS teams embedding payments directly into their product experience.

Stripe

Stripe Payouts sends funds to bank accounts and debit cards in 46 countries where Stripe supports payouts. If you already use Stripe for payment acceptance, you can tap the same API to disburse earnings to sellers or contractors.

The offering includes ACH and wire transfers in supported markets with settlement in one to five business days, instant payouts to debit cards in nine regions (capped at 10 per day and charged 1 to 1.5% per transaction), integration with Stripe Connect for marketplace split payments and seller onboarding, and API consistency with Stripe's payment acceptance products.

Stripe restricts payouts to 46 countries, charges an extra fee for instant disbursements with a daily cap, adds 1% FX markup on cross-border flows, and settles most payouts via ACH in one to five days instead of offering native real-time rails like RTP or UPI. Growing businesses need more global scale and faster settlement speeds.

Tipalti

Tipalti is an AP automation suite built for finance teams that handles supplier and contractor payments across 200 countries using about 50 payment rails.

What they offer

- Invoice processing and multi-level approval workflows that route approvals through finance hierarchies before release

- Payment delivery via ACH, wires, PayPal, and international methods with batch scheduling

- Tax compliance and reporting for suppliers, including 1099 generation and W-9 collection

- Integration with NetSuite, QuickBooks, and other ERP systems

Tipalti works well for mid-market and enterprise finance departments managing traditional supplier invoices and payments who value AP workflow automation over developer-first payout embedding.

The catch: Tipalti offers only 50 payment rails versus Dots' 300, settles payments in one to five days instead of instantly, and requires four to twelve weeks to implement compared to going live in under a week. For teams needing international payments at scale, more rails mean better coverage.

Trolley

Trolley is a payouts and tax suite that moves money to 210 countries using bank transfers, wires, PayPal, and Venmo. They support 135 currencies and include tax form collection, a white-label recipient portal, and an API for payout automation.

Trolley works for teams sending cross-border payments who can wait through a four to six week bank onboarding process and tolerate multi-day settlement windows.

The downsides: Trolley requires mandatory month-long bank onboarding before you can send your first payout, lacks instant rails like RTP and PIX, charges 2% FX spreads on cross-border transactions, and places recipient support on your internal team instead of handling inquiries directly.

Feature Comparison Table of Embedded Payout APIs

Here's how the top embedded payout APIs stack up across the features that matter most for SaaS teams:

Feature | Dots | Tremendous | Routable | Stripe | Tipalti | Trolley |

|---|---|---|---|---|---|---|

Countries Supported | 190+ | 200+ | Limited | 46 | 200+ | 210+ |

Payment Rails | 300+ | Limited | ACH/Wire | ACH/Wire/Debit | 50 | Bank/Wire/PayPal |

Real-Time Payouts | Yes | No | No | Limited (fee) | No | No |

Integration Time | Under 1 week | Days | Weeks | Days to weeks | 4-12 weeks | 4-6 weeks |

White-Label Portal | Yes | Limited | No | Limited | No | Yes |

24/7 Recipient Support | Yes | No | No | No | No | Limited |

Transparent FX Pricing | Yes | Yes | N/A | No | No | No |

Automated Tax Filing | Yes | No | No | Add-on | Yes | Yes |

API-First Design | Yes | Yes | No | Yes | No | Yes |

Why Dots Is the Best Embedded Payout API

Dots combines the broadest payment rail coverage with the fastest settlement speeds and most transparent pricing in the market. Where competitors force you to choose between global reach and instant payouts, we deliver both through 300 rails across 190 countries with real-time settlement on networks like RTP, UPI, and PIX. Our cross-border payouts API covers every market you need.

You go live in under a week instead of waiting months for bank onboarding, and your payees get white-label support directly from Dots instead of flooding your queue with payment-status tickets. With the embedded finance market growing to $622 billion by 2030, payouts are becoming a core product feature that drives retention and revenue.

We built Dots for developer teams who need to ship fast, operations leaders tired of manual processes, and CFOs who want predictable payout costs without hidden FX markups or instant-payment surcharges. Learn more about why platforms are moving beyond limited solutions.

Final Thoughts on Building With Payout APIs

Payouts are becoming a product feature and a competitive advantage, which means your developer-friendly API needs to support real-time rails and white-label experiences out of the box. You can go live in under a week with the right partner or spend months integrating legacy systems that still settle via batch ACH. The companies winning in embedded finance are the ones treating payouts as a retention driver, not a cost center.

FAQ

How do I choose the right embedded payout API for my business?

Start by mapping your must-haves: the countries you need to cover, whether your payees expect instant settlement or can wait days, and how much dev time you can invest in implementation. If you need real-time rails across 100+ countries with transparent pricing, Dots delivers all three. For simple US-only batch payouts, Stripe or Routable may suffice.

Which embedded payout solution works best for marketplace platforms?

Marketplace platforms benefit most from APIs that offer white-label onboarding, instant settlement options, and 24/7 recipient support so sellers don't flood your team with payment-status questions. Dots and Trolley both provide marketplace-specific features, though Dots ships in under a week versus Trolley's four-to-six-week bank onboarding requirement.

Can I send payouts to contractors using local payment methods like UPI or mobile money?

Yes, but rail coverage varies dramatically by provider. Dots supports 300+ rails including UPI, PIX, mobile money, and digital wallets across 190 countries, while Stripe caps coverage at 46 countries with limited instant-payout options. Check each provider's supported payment methods in your target markets before committing.

What's the difference between instant payouts and standard ACH transfers?

Instant payouts settle in seconds using real-time networks like RTP, FedNow, or UPI, while ACH transfers take one to five business days and process in batches. Some providers (Stripe, Tipalti) charge extra fees for instant delivery or cap daily volume; Dots includes real-time settlement at no surcharge wherever the rail supports it.

When should I switch from manual payout processing to an embedded API?

If your team spends more than ten hours per week managing spreadsheets, answering payment-status tickets, or manually filing tax forms, or if you're scaling beyond one country, an embedded payout API will save time and reduce errors. Most SaaS teams see ROI within the first month after switching from manual workflows.