Global Payouts: The Complete Guide for Businesses in April 2026

Paying freelancers in ten different countries means ten different banking requirements, currency conversions, and compliance checks. Most companies start with Stripe payout api setups and quickly hit walls around local payment methods or hidden FX spreads. We're showing you how global payout infrastructure actually works, from identity verification to final settlement, so you can cut friction and speed up transfers without absorbing unexpected costs.

TLDR:

- Global payouts route funds to contractors in 190+ countries via local rails like mobile money and wallets

- Real-time networks settle in seconds; ACH and wires take 1-5 days and often add FX markup fees

- Compliance demands KYC checks and tax forms like W-9 or W-8BEN before you can send cross-border funds

- Stripe covers 46 countries; alternatives support 300+ rails without daily caps or instant-payout surcharges

- Dots moves $1.5bn annually with instant settlement, automated tax filing, and zero hidden conversion fees

What Are Global Payouts?

Sending money internationally creates headaches when you rely on slow bank wires. Global payouts are the financial systems businesses use to distribute funds to overseas contractors, marketplace sellers, and affiliates.

Distributed work is the default setting in 2026. How do you reliably route earnings to workers across multiple countries? You can execute global mass payouts through one API connection to move funds across borders automatically.

Behind the scenes, these systems connect your business to local payment rails in each country, routing funds through the fastest, most cost-effective path available.

How Global Payout Systems Work

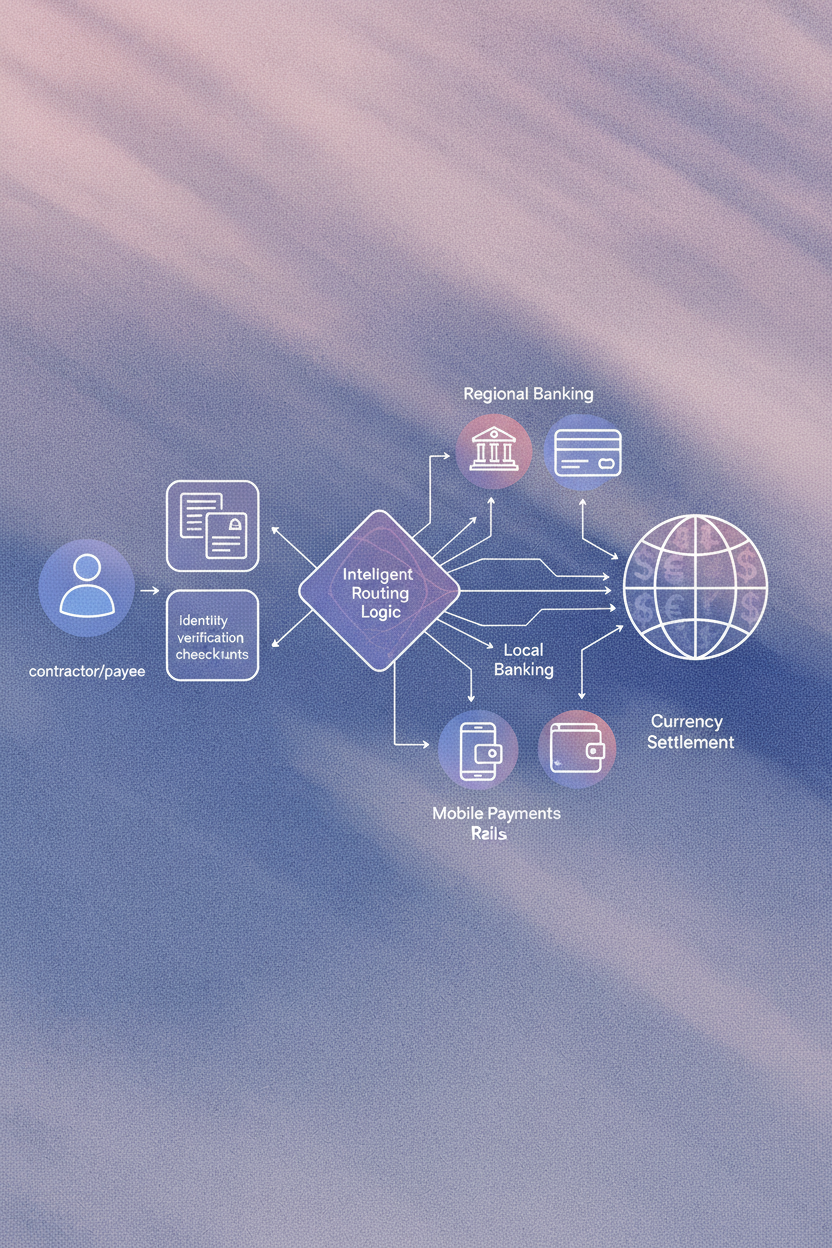

Sending money across borders securely demands a precise workflow. The sequence starts the moment a contractor requests their earnings.

First comes payee onboarding. You must collect financial details and clear mandatory compliance checks like Know Your Customer (KYC) before funds move. Once verified, routing logic assumes control.

Executing international transfers requires linking identity verification directly to local payment rails.

While the Stripe global payouts API handles basic workflows, intelligent routing adapts to local rails, compliance requirements, and real-time settlement windows across every region.

Key Components of a Global Payout Infrastructure

Building global payout infrastructure requires specific moving parts. Every piece changes transfer speed, total costs, and payee experience. The global cross-border payments market reached $1 quadrillion in 2024, demanding solid infrastructure to handle complexity at scale.

Global Payout Methods and Payment Rails

The traditional and crypto payment market hit roughly one quadrillion dollars in 2024. Global real-time payments reached 266.2 billion transactions in 2023, a 42.2% increase. Match global payouts to payee geography, speed, and budget. We route funds across all options.

Category | Examples | Speed | Ideal Use |

|---|---|---|---|

Bank Transfers | ACH, SEPA, SWIFT | 1-5 business days | High-value payouts in North America and Europe where contractors expect traditional banking |

Real-Time Networks | RTP, FedNow, PIX, UPI | Seconds to minutes | Urgent disbursements and markets where instant settlement drives retention |

Mobile Money | M-Pesa, MTN Mobile Money, Orange Money | Instant to 2 days | Africa and Southeast Asia where mobile wallets dominate local commerce |

Digital Wallets | PayPal, Venmo, Cash App | Instant to 2 days | Gig workers and small payouts where payees already hold active wallet accounts |

Card Disbursements | Visa Direct, Mastercard Send | Minutes to 1 day | Emergency payouts and regions with limited banking infrastructure |

Regional Considerations for Global Payouts

Treating every region exactly the same guarantees failed transfers. A successful approach to global payouts requires local context.

Payees in North America and Europe expect direct bank transfers.

In Africa or Southeast Asia, mobile money is the default choice. Africa's mobile money market share totaling $2.09 trillion in 2025, with mobile money penetration exceeding 60% in countries like Uganda and Tanzania where traditional banking reaches only 43% of adults.

Forcing contractors into unfamiliar payment methods causes friction and delays earnings.

Jurisdiction rules control how fast you route funds. Compliance varies by country. Real-time payment options settle in seconds, but Stripe's coverage focuses on 46 countries. If your contractors work across developing markets, you'll need broader rail access to avoid forcing them into slower, costlier alternatives.

Compliance and Tax Requirements for International Payouts

Sending cross-border funds introduces strict regulatory obligations. Before routing money, you must pass Know Your Customer and Anti-Money Laundering checks. Every payee needs vetting against sanctions lists like OFAC.

Tax rules add another hurdle. Depending on location, you must collect W-9, W-8BEN, or T4A forms. Miss the proper withholding amount, and your business absorbs the tax penalties and compliance risks.

Payout Speed and Settlement Timelines

Waiting for funds frustrates contractors. Payment speed directly impacts worker retention.

Your chosen method alters settlement timelines:

- ACH clears in one to three business days.

- Wire transfers take one to five days globally.

- Real-time networks finish in seconds.

- Wallet disbursements arrive instantly or require two days.

Contractors often ask, does Stripe payout on weekends? Standard Stripe payouts follow banking schedules and don't process on weekends or holidays, though instant payouts arrive seven days a week for an additional fee.

Cost Structure of Global Payouts

Cross-border transfers carry hidden fees. You need a clear view of these economics because transaction costs directly impact your profit margins.

Expect four common charges:

- Base transfer fees cover the actual movement of your funds.

- Foreign exchange spreads introduce hidden conversion markups during currency switches.

- Intermediary banks take unexpected cuts along correspondent routing paths.

- API usage costs charge you per transaction and compound quickly at scale.

Stripe Payouts Overview

Developers often consult the Stripe global payouts docs first. Fast international transfers shape the future of money movement.

The Stripe payout schedule controls when your funds clear. Learning how to change Stripe payout frequency gives you more control over cash flow, though daily limits and instant-payout fees often offset that flexibility.

Common Challenges in Global Payout Operations

Scaling international disbursements causes severe friction. Diagnose these roadblocks early to pick the right payouts company.

- Bad currency conversion rates add hidden costs that erode margins quickly at volume.

- Limited payment rail coverage forces contractors into slower, costlier alternatives they don't use.

- Incomplete compliance workflows expose your business to regulatory penalties and blocked transfers.

- Manual reconciliation processes create bottlenecks when you need to track thousands of disbursements.

- Poor API documentation and integration support delay launches and prevent scaling.

How to Choose a Global Payout Provider

Selecting the right payouts company prevents delayed earnings and keeps contractors satisfied. Build your vendor scorecard around these infrastructure requirements.

- Verify they support preferred local payment methods across your target countries, beyond standard bank transfers.

- Review their tech speed. Integrating a flexible stripe payout api alternative should take days, not months.

- Demand clear terms. Always compare stripe global payouts pricing against vendors offering zero hidden markups.

- Confirm the provider handles compliance automatically, including KYC verification and tax documentation collection.

- Confirm they offer instant settlement options and real-time tracking so you can monitor disbursement status across all payment rails.

- Test their reporting capabilities to verify you can match payments and track disbursement status in real time.

Building a Scalable Global Payout Strategy with Dots

Tired of managing broken international transfers? Dots solves this complexity. You can replace a restrictive Stripe global payouts API setup with a payout orchestration integration that handles identity verification and final settlement.

Our connection brings complete payment coverage:

- Access over 300 payment rails across more than 190 countries for global reach.

- Deliver real-time settlement via RTP, FedNow, PIX, UPI, and other instant networks.

- Support local payment methods including mobile money, digital wallets, and card disbursements.

- Automate compliance with built-in KYC verification, sanctions screening, and tax form collection.

- Eliminate hidden fees with transparent pricing and zero FX markups on currency conversions.

- Track every transaction through unified reporting and reconciliation dashboards.

Final Thoughts on Cross-Border Fund Distribution

Sending earnings to international teams shouldn't require manual processes and long settlement windows. Stripe global payouts alternatives give you more payment options and better coverage across developing markets. You control costs when transparent pricing replaces hidden FX markups and intermediary fees. Dots handles verification, routing, and settlement in one connection. Contact our team to see the difference.

FAQ

How long does it take to settle a global payout?

Settlement speed depends on your payment method. Real-time networks like RTP, FedNow, PIX, and UPI deliver funds in seconds, while ACH takes one to three business days and wire transfers can take one to five days globally.

What payment methods do payees actually prefer in different regions?

North America and Europe expect direct bank transfers, while Africa and Southeast Asia default to mobile money. Forcing contractors into unfamiliar methods creates friction and delays, so match the payment rail to local preferences.

Do I need to collect tax forms for international contractors?

Yes, tax obligations depend on payee location and your jurisdiction. You must collect W-9 forms for U.S. workers, W-8BEN for international contractors, or T4A for Canadian payees, and handle proper withholding to avoid absorbing tax penalties yourself.

What hidden fees should I watch for in cross-border transfers?

Expect four common charges: base transfer fees, foreign exchange spreads that hide conversion markups, intermediary bank cuts along correspondent routing paths, and API usage costs that compound at scale.

Can I route payouts through multiple payment rails automatically?

Yes, modern payout infrastructure uses routing logic to select the best rail based on payee location, speed requirements, and cost. Dots supports over 300 payment methods across 190+ countries through a single API connection.