Marketplace Payment API: Complete Guide for Businesses in April 2026

Every time a customer checks out on your site, the money lands in your account and you owe a percentage to the seller. A stripe connect alternative or any solid marketplace payment API divides that transaction automatically so you never touch a manual transfer form again. Most operators realize too late that standard processors only handle the buyer side, leaving you to settle up and pay vendors on your own. This guide covers how split payment architecture works, what compliance checks you need, and how long integration actually takes when you pick the right tools.

TLDR:

- Marketplace payment APIs split funds between sellers and your business instantly

- Real-time rails move money in seconds vs 1-3 days with ACH/wire transfers

- Hidden fees cut a 12% commission down to 6-8% after card networks and FX markups

- Basic API setups go live in under a week; custom flows take 2-4 weeks

- Dots moves $1.5bn yearly across 300+ rails in 190 countries with instant payouts

What Is a Marketplace Payment API

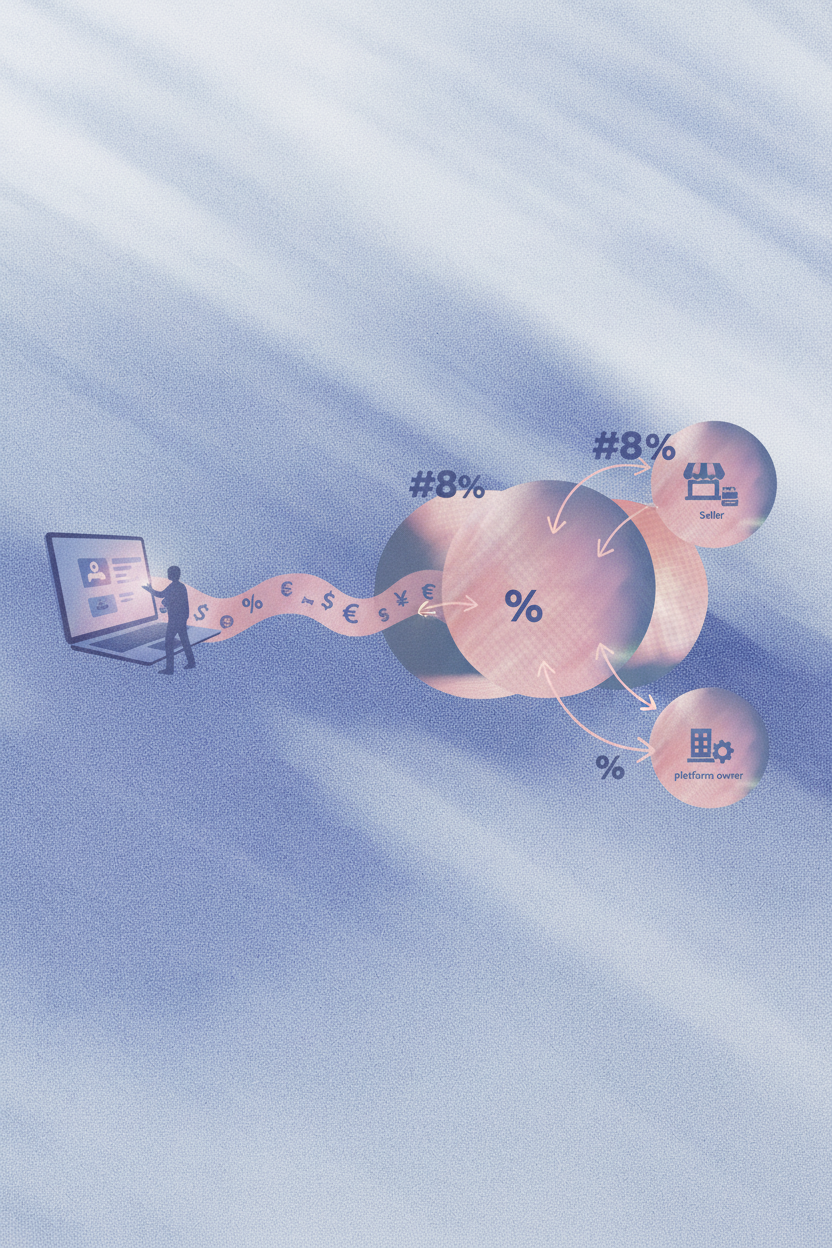

When you run a digital marketplace, moving money gets complicated fast. Standard checkout flows work perfectly for simple setups where customers pay you directly. Do you really want to process thousands of separate transfers by hand? Multiparty transactions demand different infrastructure because buyers purchase goods, sellers need their cut, and you must collect your fee.

A marketplace payment API acts as the financial engine directing these complex money movements.

How Marketplace Payment APIs Work

When a customer buys a service on your site, the marketplace payment infrastructure executes a quick sequence of background events. You need an architecture that manages authorization, capture, and multiparty routing simultaneously. Getting each step right protects both buyers and sellers from failed or misdirected payments.

Transaction Initiation

A marketplace payment gateway verifies the buyer has sufficient funds. This step holds the money securely.

Split Logic Routing

Once approved, the system captures the charge and divides the total. Custom API rules let you define exactly how much each party receives based on your business model.

Split Payment Architecture and Implementation

Dividing incoming funds manually causes scaling problems. An effective API divides transactions between your business and your payees automatically in real time.

- Fixed commissions involve taking a set dollar amount from every sale. The payouts API calculates this instant deduction before routing the remaining balance to the vendor.

- Variable commissions let you charge a percentage based on transaction size or category. The code reads your custom parameters and executes the split instantly, adjusting your take rate dynamically per transaction.

Managing Marketplace Payouts at Scale

Sending money across borders creates headaches as your user base grows. You must route funds through localized banking networks and manage multiple currencies to keep payees satisfied. Payout timing directly drives retention. You can configure scheduled batches for predictable cash flow or trigger instant deposits to attract top earners.

Manually verifying global transactions destroys productivity. By automating your disbursement cycle with top marketplace payment solutions, your finance team avoids tedious reconciliation work and can focus on growth initiatives instead of chasing down individual transfer confirmations.

API Integration Timeline and Requirements

Planning your technical sprint requires realistic expectations. Building your financial engine does not have to drain engineering resources for months. Basic setups go live in under a week. Custom onboarding flows handling multiple currencies take two to four weeks. Most developers work through a sandbox environment first, running test transactions to confirm split logic fires correctly before touching live funds. Once sandbox testing passes, flipping to production typically takes a single configuration change and a compliance review sign-off from your team.

Before writing code, grab the right tools. Developers start by reading the marketplace payment API documentation to map out endpoints. With sandbox access, they generate secure keys to test the logic. You might need your legal team to review terms of service and your finance team to configure your commission structure before flipping your integration to production mode.

Compliance and KYC Requirements for Marketplaces

Manual verification stalls revenue. Automated compliance tools remove friction and cut payee onboarding dropouts by 20% to 40%. Dots packages tax collection and identity checks into one API. Every payee gets screened against global watchlists at onboarding. The system collects W-9 and W-8BEN forms automatically, then generates 1099s at year end without your team touching a spreadsheet. Staying current with country-specific tax rules no longer requires a dedicated compliance hire.

Real-Time Payment Rails vs Traditional Settlement

Waiting for legacy ACH and wire transfers to clear causes friction. Old settlement cycles hold funds for one to three business days. Speed now drives loyalty. Research shows that 62% of sellers abandon a marketplace if competitors offer faster payouts.

Payment Solution | Settlement Speed | Global Rail Coverage | Integration Timeline | Instant Payout Fees | Multi-Party Split Logic |

|---|---|---|---|---|---|

Dots | Real-time via RTP, FedNow, PIX, UPI with instant settlement in seconds | 300+ payment rails across 190 countries with single API integration | Basic setup in under one week; custom flows in 2-4 weeks | No additional fees for instant payouts included in standard rates | Built-in automated split payment architecture with custom commission rules |

Stripe Connect | Standard ACH takes 2-7 business days; instant payouts available for additional fee | Supports 46+ countries with varying payment methods per region | Basic integration 1-2 weeks; complex marketplace flows 4-8 weeks | Additional 1-1.5% fee per instant payout on top of standard processing | Separate Accounts and Transfers required; more complex implementation |

Traditional Wire/ACH | ACH: 1-3 business days; Wire: same day to 1 business day | Limited to domestic transfers; international wires require correspondent banking | Manual setup with banking partner; no API integration | Not applicable; no instant payout capability | Requires manual calculation and separate transactions for each party |

PayPal for Marketplaces | Standard transfers take 1-3 business days; instant available with fee | 200+ countries but limited local payment method support | Integration typically 2-3 weeks for basic marketplace setup | 1% fee for instant transfers capped at $10 per transaction | Mass Pay and adaptive payments with API-driven split configuration |

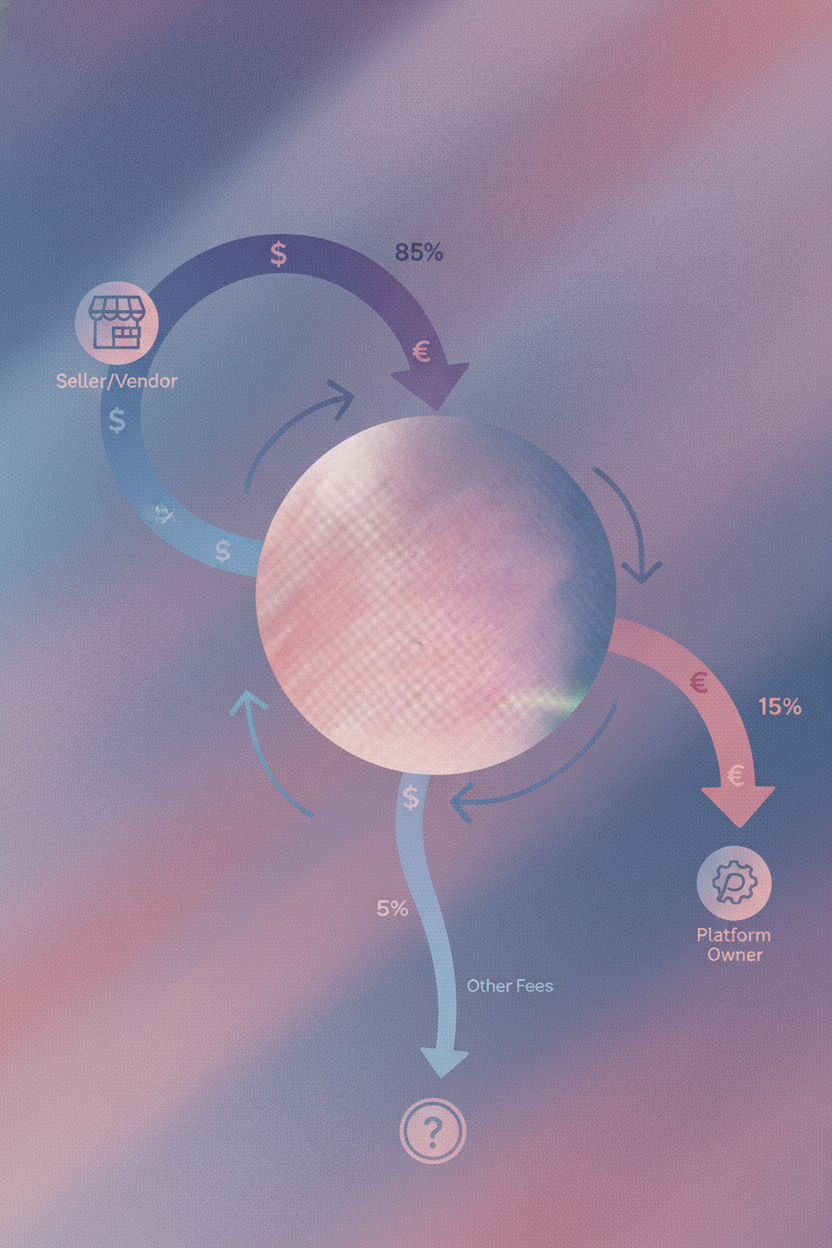

Calculating Your Effective Take Rate

Setting a 12% commission seems like a great revenue strategy. Hidden expenses quickly erode expected margins. Card networks take an immediate cut at checkout. Disbursing funds globally drains balances further through exchange markups.

Operators realize late that unforeseen processing fees shrink actual profits to just 6-8% of the original 12% commission after card network fees, FX markups, and payout costs stack up.

Building Marketplace Payments With Dots

Manual transfers drain your finance team. Clinging to outdated routines means hiring more staff to process payouts.

Automating payout infrastructure lets your business grow without adding operations headcount.

We built Dots to solve these exact headaches. Your developers can integrate our single API using minimal code. This setup takes under one week to complete. You instantly access 300+ payment rails across 190 countries, moving $1.5 billion annually through a single integration that handles everything from real-time transfers to traditional ACH, all without the markup fees that legacy providers stack on top.

Final Thoughts on API-Driven Payment Splits

Manual payout processes break down fast once you pass a few hundred transactions per month. An online payment solution with built-in split logic removes that bottleneck and lets you route funds in real time. Your developers can ship a working integration in under a week, and your finance team stops chasing wire confirmations. Get in touch with us to see what automating your marketplace payments with Dots looks like.

FAQs

What's the difference between a marketplace payment API and a standard payment processor?

A standard processor handles simple buyer-to-merchant transactions, while a marketplace payment API automatically splits funds between multiple parties. It routes money to sellers, collects your commission, and manages payouts across different currencies and payment rails.

How long does it take to integrate a marketplace payment API?

Basic setups go live in under one week, while custom implementations with multi-currency support and specialized onboarding flows typically take two to four weeks depending on your requirements.

Can I offer instant payouts without paying extra fees per transaction?

Yes, modern APIs like Dots include real-time payment rails (RTP, FedNow, PIX, UPI) by default without charging the 1-1.5% instant payout fees that legacy providers add on top of their standard rates.

Why does my 12% commission shrink after processing fees?

Card network fees, currency exchange markups, and payout costs eat into your gross commission. A 12% rate can drop to 8-9% after accounting for these hidden expenses, making it critical to calculate your effective take rate before setting pricing.

What compliance checks do I need before paying sellers internationally?

You need KYC (Know Your Customer) identity verification for all payees, plus country-specific tax documentation. Automating these checks through your API cuts onboarding dropouts by 20-40% compared to manual verification processes.