The Rise of Embedded Payouts: Why Every Vertical SaaS Needs Payout Infrastructure in March 2026

Everyone's talking about the rise of embedded payouts, but here's what actually changed. Five years ago, letting users pay contractors inside your vertical SaaS was a differentiator. Today, it's the baseline. If you can't pay people inside your product, you're losing deals to competitors who can. The shift happened fast because the payout side is harder than pay-ins. Different rails, compliance layers, tax filing, fraud checks, recipient support. That complexity is exactly why payouts are now infrastructure, not a feature. Freelance marketplaces, creator tools, affiliate networks, and gig apps all compete on how fast and how widely they can pay people. If you bolt on a basic ACH tool and call it done, you're already behind competitors offering same-day transfers to 100 countries.

TLDR:

- Vertical SaaS platforms that embed payouts capture transaction revenue far exceeding subscription fees

- 74% of consumers now expect instant payouts; 57% who try them make it a habit

- Over 70% of freelancers would switch platforms for better payment experiences

- Automated compliance and tax filing lets you scale payees without adding ops headcount

- Dots offers instant payouts across 300+ rails in 190+ countries with built-in tax automation

Why Embedded Payouts Are Shifting From Feature to Infrastructure

Five years ago, if your vertical SaaS let users pay contractors or sellers, that was a nice-to-have. Today, if you can't pay people inside your product, you're losing deals to competitors who can.

The shift happened fast. Embedded payments crossed into the mainstream when transaction value hit $25 trillion. But most of that headline number tracks pay-ins: card processing, checkout flows, subscription billing. The payout side stayed fragmented longer because moving money out is harder. Different rails, compliance layers, tax filing, fraud checks, recipient support.

That complexity is exactly why payouts are now infrastructure, not a feature. Your users expect to collect payment and disburse earnings without leaving your software. Freelance marketplaces, creator tools, affiliate networks, gig apps all compete on how fast and how widely they can pay people. If you bolt on a basic ACH tool and call it done, you're already behind competitors offering same-day transfers to 100 countries.

Payouts are table stakes. The question is whether you build or buy the rails underneath.

The Revenue Opportunity in Payout Infrastructure

Vertical SaaS companies typically chase annual recurring revenue from software seats. But the bigger prize sits in the transaction layer. When you own payouts, you capture a slice of every dollar that flows through your product.

The math is compelling. Embedded finance transaction volume in the U.S. is expected to exceed $7 trillion by 2026, up from $2.6 trillion in 2021. Even a small take rate on that volume dwarfs subscription revenue. If your vertical SaaS processes $500 million in annual payouts and you charge 50 basis points, that's $2.5 million in new revenue without adding a single new customer.

Attachment rates matter too. Toast, the restaurant point-of-sale company, generates more revenue from payments than from software. The pattern repeats across verticals: once users trust you to run their business, they'll trust you to move their money. Payout infrastructure turns every transaction into a recurring revenue event.

The shift from software-only to software-plus-payouts isn't about adding a new SKU. Companies that integrate financial services see higher retention, lower churn, and deeper product stickiness. When your users depend on you to pay their people, switching costs skyrocket.

Metric | Traditional Payouts | Embedded Payout Infrastructure |

|---|---|---|

Revenue Model | Software subscriptions only | Software + transaction fees (50+ basis points) |

Payout Speed | 3-5 business days (ACH batches) | Instant to same-day delivery |

Geographic Coverage | Limited to 10-20 countries | 190+ countries, 300+ payment rails |

Compliance Management | Manual tax form collection and filing | Automated W-9/1099 collection and filing |

User Retention Impact | Standard SaaS churn rates | Higher retention due to payment lock-in |

Ops Headcount | 1 person per few thousand payees | Scales without proportional headcount growth |

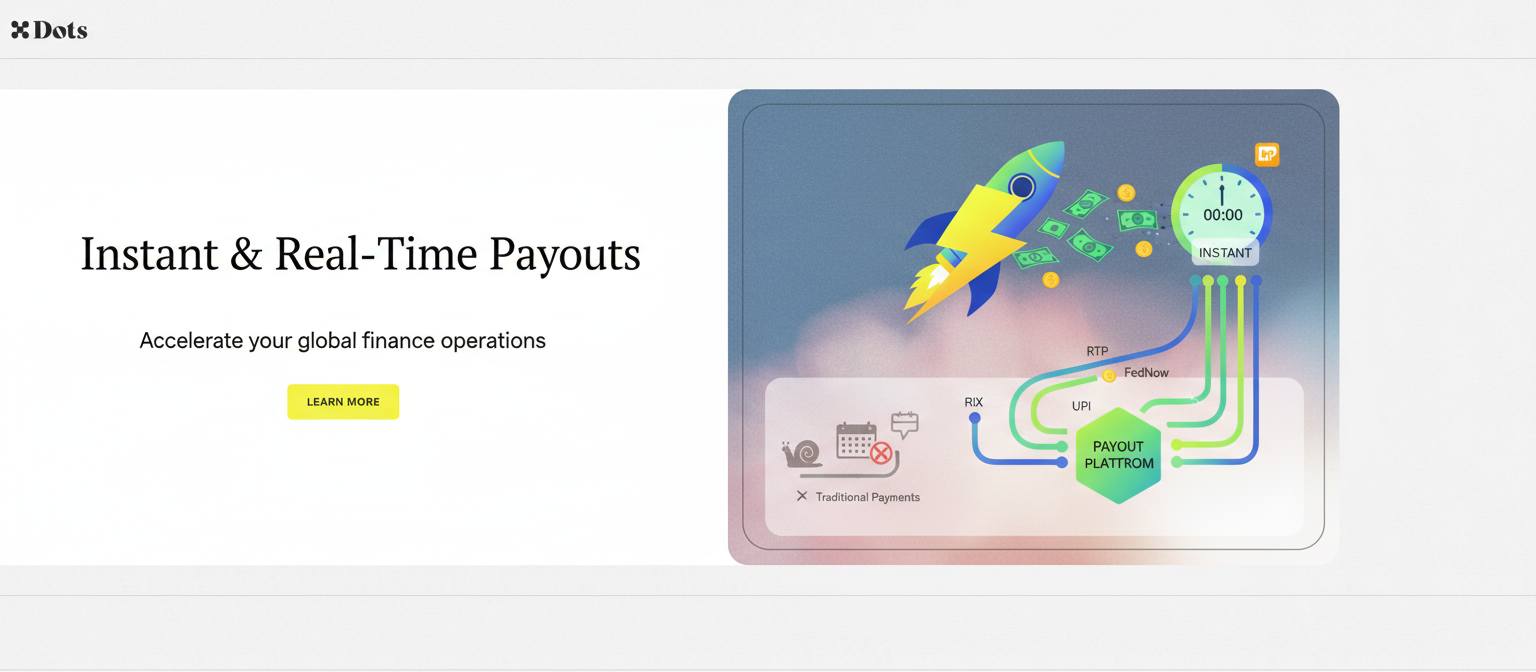

Real-Time and Instant Payouts Become Table Stakes

Speed used to be a competitive advantage in payouts. Now it's the baseline.

Gig workers, contractors, and creators expect immediate access to their earnings. The behavioral shift is measurable: nearly three in four consumers have now received at least one instant payout. That's no longer early adopter territory. Instant delivery has hit mainstream scale.

The stickiness is even more telling. Fifty-seven percent of consumers who try instant payouts make them a habit. Once someone gets paid in seconds instead of days, they rarely accept the old way again. If your competitor offers same-day deposits and you're still batching ACH transfers overnight, you're creating churn.

Real-time rails like RTP and FedNow in the U.S., UPI in India, and PIX in Brazil make instant payouts possible without custom integrations. The infrastructure exists. The question is whether your payout stack can tap into it across markets without rebuilding your API for every country.

If you're still treating speed as optional, your users are already looking elsewhere.

Global Payout Coverage Separates Winning Platforms

Your contractor base spans dozens of countries now. Limited payout coverage is costing you users.

Over 70% of independent workers said they would leave their current freelancer marketplaces for better payment experiences. With 1.57 billion people earning income from freelance work worldwide, that's a massive pool of users making decisions based on how well you pay them.

The issue goes beyond currency conversion. A bank transfer works in Germany, but your contractor in Kenya needs M-Pesa. Your seller in Brazil expects PIX. Your creator in the Philippines wants GCash. If you only offer wire transfers or PayPal, you're forcing people into expensive, slow rails that eat into their earnings.

Multi-country coverage is now a retention metric. When a competitor supports the local payment method your user actually wants, they switch. The friction isn't your software: it's the last mile, getting money into the account or wallet they use every day.

Payout reach separates winning vertical SaaS products from the ones watching users churn to competitors with better rails.

Compliance and Tax Automation Unlock Scalability

Scaling payouts from 100 payees to 10,000 multiplies transaction volume and creates an exponential compliance burden.

Every new contractor requires a W-9 collected, validated, and stored. Every international payee triggers KYC checks. Every payout over $600 requires a 1099 filed with the IRS. Manual spreadsheets and follow-ups cause your ops team to drown long before you hit scale.

Tax season support tickets spike when payees can't find their forms or you miss a filing deadline. Each manual compliance check adds friction. Each missed OFAC screening creates legal risk. Operations teams that scale manually hire one support person for every few thousand payees just to handle paperwork.

Automated payout infrastructure flips that ratio. Systems that collect tax forms during onboarding, validate information in real time, and file 1099s programmatically remove the bottleneck. KYC and sanctions screening happen at the API level. When a payee needs their tax form, the system sends it instantly instead of routing through support.

This changes everything for ops. Compliance automation lets you grow your payee base without proportional headcount growth. Your ops team moves from chasing forms to handling exceptions, and your legal team stops worrying about missed filings.

How Dots Builds Payout Infrastructure for Vertical SaaS

We built Dots to solve these problems. RTP and FedNow support delivers instant payouts without surcharges. 300+ rails across 190+ countries mean your payees get funds through the methods they actually use, whether that's UPI, PIX, M-Pesa, or bank wires.

Tax automation handles W-9 collection, validation, and 1099 filing through the API. White-label onboarding flows keep your brand visible at every touchpoint. Integration takes under a week because the stack is purpose-built for developers.

Vertical SaaS companies, marketplaces, gig apps, and creator tools use Dots when payouts need to feel like a core product feature, not a vendor handoff. You own the experience while we handle the rails, compliance, and recipient support underneath.

Final Thoughts on Why Vertical SaaS Needs Payout Infrastructure

Your users won't forgive slow payouts or limited country coverage when competitors offer instant deposits worldwide. Building payout infrastructure in-house means hiring compliance specialists, integrating 300+ payment rails, and automating tax filing across jurisdictions. Or you can plug into infrastructure that already does all of that and ship payouts in under a week. We built Dots for vertical SaaS teams who want to own the experience without building the pipes underneath.

FAQ

How do instant payouts improve user retention?

Once someone receives an instant payout, 57% make it a habit and rarely accept slower methods again. If your competitor offers same-day deposits and you're batching ACH transfers overnight, you're creating churn before users even consider your software features.

What is the revenue difference between software-only and software-plus-payouts models?

If your vertical SaaS processes $500 million in annual payouts at 50 basis points, you generate $2.5 million in new revenue without adding a single customer. Companies like Toast now earn more from payments than software subscriptions because every transaction becomes a recurring revenue event.

When should I automate tax compliance for payouts?

When you're scaling past a few hundred payees, manual compliance becomes a bottleneck. Every payout over $600 requires a 1099 filed with the IRS, and operations teams typically hire one person for every few thousand payees just to handle paperwork without automation.

Why do contractors leave platforms over payment options?

Over 70% of independent workers said they would leave their current marketplace for better payment experiences. A bank transfer works in Germany, but your contractor in Kenya needs M-Pesa and your seller in Brazil expects PIX. Limited rail coverage directly drives user churn.

Can I integrate payout infrastructure without rebuilding my product?

Yes. Modern payout APIs take under a week to integrate because they handle rails, compliance, tax filing, and recipient support through a single REST interface. You keep your brand experience while the infrastructure runs underneath.