What Is a Digital Wallet and How Does It Work in March 2026?

Your phone already holds your boarding passes, event tickets, and loyalty cards. Digital wallet apps turned it into your payment method too, and now billions of people worldwide tap to pay instead of swiping plastic. The tech behind it goes deeper than convenience, with tokenization and encryption working invisibly every time you check out. We'll break down how these apps store your payment info, keep it secure, and why they're becoming the preferred way for businesses to send payouts.

TLDR:

- Digital wallets store payment info securely on your phone, letting you pay with a tap or click.

- Tokenization replaces your card number with single-use codes that expire after each transaction.

- 69% of U.S. adults used a digital wallet in the past 30 days; volume will hit $17 trillion by 2029.

- Wallets are safer than physical cards because your real account number never reaches merchants.

- Dots connects you to 300+ payout methods, including every major digital wallet, through one API.

What Is a Digital Wallet?

A digital wallet is a software app that securely stores your payment information in one place. Instead of carrying physical cards, you keep credit cards, debit cards, bank account details, and other payment methods on your phone or computer.

Think of it as a virtual version of your leather wallet, but with added security and convenience. When you make a purchase online or in person, the wallet retrieves your stored payment data and completes the transaction in seconds.

Digital wallets have come a long way since PayPal launched in the late 1990s. What started as a tool for online auctions has grown into a global payment method. Today, billions of people use apps like Apple Pay, Google Wallet, and Cash App to buy coffee, split bills, or shop online.

How Digital Wallets Work

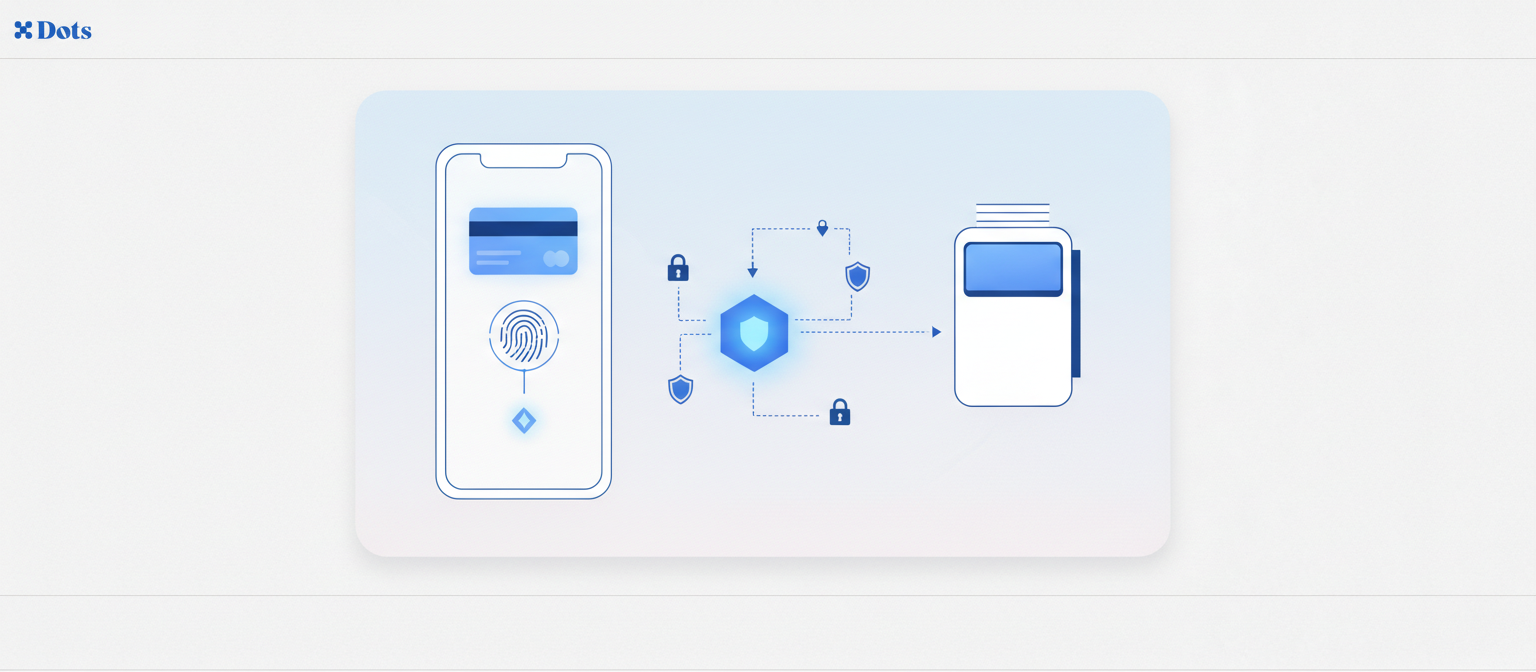

Setting up a digital wallet takes about two minutes. You download the app, then add your payment method by snapping a photo of your card or typing in the details manually. The wallet encrypts this information and stores it on your device or in the cloud.

When you're ready to pay, you open the app and authenticate yourself. Most wallets use biometric verification like Face ID or fingerprint scanning. Some ask for a PIN or passcode instead. This step confirms you're the account owner before releasing any payment data.

Instead of sending your actual card number to the merchant, the wallet creates a unique token for that specific transaction. The token acts as a stand-in that expires after use, so even if someone intercepts it, they can't steal your real payment details.

Types of Digital Wallets

Digital wallets fall into three main categories based on how you use them. Mobile wallets like Apple Pay, Google Pay, and Samsung Pay live on your phone and use NFC technology for tap-to-pay transactions at physical stores. Online wallets such as PayPal, Venmo, and Cash App focus on web checkouts and peer-to-peer transfers. Cryptocurrency wallets hold Bitcoin, Ethereum, and other digital currencies through hardware devices, mobile apps, or browser extensions that store private keys.

Another way to group wallets is by acceptance. Open wallets work anywhere the payment network operates. Semi-closed wallets limit you to specific merchants or locations. Closed wallets tie you to a single company's ecosystem.

How Tokenization Keeps Digital Wallets Secure

When you tap your phone at checkout, tokenization swaps your card number for a single-use code before the transaction leaves your device. Merchants receive a 16-digit string that looks like a credit card number but expires within seconds. Even if someone intercepts that data, it's useless for future purchases.

Each token links to your specific phone, so copying the code to another device won't work. 5.2 billion people are expected to use digital wallets by 2026, making this invisible security layer critical. Your real account number stays locked in secure servers and never reaches the store or website processing your payment.

Digital Wallet Adoption and Growth in 2026

Digital wallets have shifted from niche to norm. 69% of U.S. adults used a digital wallet in the past 30 days, reflecting widespread acceptance across demographics. You see them everywhere: tap-to-pay at registers, instant bill splits through apps, one-click online checkouts without entering card details.

$17 trillion in volume by 2029, climbing 11.2% annually. Retailers are adding digital wallet acceptance because customers demand it. The reason for ongoing adoption is straightforward: wallets remove friction by eliminating manual card entry, reducing physical dependencies, and keeping payment credentials off merchant servers. Speed and security gains multiply across every transaction.

Benefits of Digital Wallets for Consumers

You skip the fumble at checkout. No digging through your bag for the right card, no typing 16 digits into a tiny form field. One tap or click closes the transaction. That speed compunds when you're buying groceries, booking rides, or checking out across multiple sites in a day.

Security improves because your card number never reaches the cashier or website. Biometric login blocks anyone else from accessing your wallet, even if they grab your phone. You get instant alerts for every charge, so suspicious activity surfaces within seconds instead of weeks later on a paper statement.

Beyond payments, wallets store boarding passes, event tickets, and loyalty cards. Transaction histories appear in one feed, making it easier to track expenses and manage budgets without spreadsheets or receipt piles.

Are Digital Wallets Safe?

Multiple security layers protect your wallet at every step. End-to-end encryption scrambles your data during transmission, so intercepted signals are unreadable. Multi-factor authentication requires your face, fingerprint, or PIN before releasing payment data, blocking unauthorized users even if they access your unlocked phone.

If your device disappears, remote-wipe features let you erase wallet contents from any browser. Most apps also let you freeze or delete individual cards without calling your bank.

To maximize protection, set up biometric locks and skip auto-login. Review transaction alerts immediately and report anything strange. Avoid public Wi-Fi for wallet activity, and keep your phone's operating system updated.

Digital wallets are safer than physical cards because stolen tokens expire and your real account number stays hidden.

Using Digital Wallets for Business Payouts

Businesses send earnings to contractors and gig workers through the same wallets used for everyday purchases. Instead of waiting three to five days for a bank transfer, payees receive money in their PayPal, Venmo, or Cash App account in minutes.

This shift matters when paying freelancers who need immediate access to earnings or creators who prefer collecting through Cash App instead of waiting for a direct deposit. Someone driving for a rideshare app or completing micro-tasks wants their earnings now, not next Tuesday. Offering wallet payouts alongside bank transfers and debit cards lets payees choose what works best for them.

How Dots Simplifies Digital Wallet Payouts at Scale

When you need to send digital wallet payouts at scale, integrating each app individually consumes engineering resources and multiplies compliance work. Dots connects you to 300+ payout methods through a single API, including every major digital wallet.

Your payees select their preferred wallet during onboarding. We route payments, manage tax collection, and settle funds instantly. Whether your contractor chooses Cash App and your freelancer picks PayPal, both receive money in seconds through one integration. No custom code per wallet, no settlement delays, no fragmented compliance tracking.

Popular Digital Wallet Examples

Apple Pay and Google Pay dominate in-store tap payments. Apple Pay works exclusively on iPhone, iPad, Apple Watch, and Mac devices. Google Pay runs on Android phones and works across most NFC terminals. Both let you hold multiple cards and switch between them inside the app.

Cash App and Venmo specialize in splitting bills and sending money to friends. Cash App offers a debit card and direct deposit routing, turning the app into a lightweight checking account. Venmo adds a social feed where you can share payment activity with friends.

PayPal handles online checkouts and invoicing for freelancers and small businesses. The app connects to your bank or card, then speeds up web purchases with one-click confirmation.

MetaMask and Coinbase Wallet store cryptocurrency and NFTs. MetaMask runs as a browser extension or mobile app for Ethereum and compatible blockchains. Coinbase Wallet operates separately from the Coinbase exchange, giving you full control of your private keys.

Digital Wallet | Device Type | Primary Use Case | Key Features |

|---|---|---|---|

Apple Pay | iOS, macOS, watchOS | In-store tap payments | NFC payments, biometric authentication, works across Apple devices |

Google Pay | Android, Web | In-store and online payments | NFC payments, loyalty card storage, works on most Android phones |

PayPal | Web, iOS, Android | Online checkouts, invoicing | Buyer protection, international transfers, merchant integration |

Cash App | iOS, Android | P2P transfers, direct deposit | Debit card, Bitcoin trading, stock investing |

Venmo | iOS, Android | Social payments, bill splitting | Social feed, instant transfers, Venmo debit card |

MetaMask | Browser extension, iOS, Android | Cryptocurrency storage | Ethereum and ERC-20 tokens, dApp integration, private key control |

Final Thoughts on Digital Wallet Payouts

Wallets went from niche tech to your default payment method in less than a decade. The benefits of digital wallets stack up: faster checkouts, better security, instant notifications. When you're paying hundreds of freelancers who each prefer different apps, you need infrastructure that routes money to Cash App, PayPal, Venmo, and everything else without custom code for each one.

FAQ

How do digital wallets protect my actual card number during transactions?

Digital wallets use tokenization to swap your real card number for a single-use code before the payment leaves your device. Merchants only see this temporary token, which expires after one transaction, so your actual account details never reach the store or website.

What's the difference between mobile wallets and online wallets?

Mobile wallets like Apple Pay and Google Pay live on your phone and use NFC technology for tap-to-pay at physical stores, while online wallets such as PayPal and Cash App focus on web checkouts and peer-to-peer money transfers between friends or family.

Can businesses pay contractors through digital wallets?

Yes, you can send payments directly to contractors' Cash App, PayPal, Venmo, or other wallet accounts instead of waiting three to five days for traditional bank transfers. Payees receive their earnings in minutes and can choose their preferred wallet during onboarding.

When should I use a cryptocurrency wallet versus a regular digital wallet?

Cryptocurrency wallets like MetaMask and Coinbase Wallet are built to hold Bitcoin, Ethereum, and other digital currencies with private key storage, while regular digital wallets like Apple Pay or Google Pay handle traditional payment methods like credit cards and bank accounts for everyday purchases.